Election Volatility - Part 2

Rotational Forces & "Funding Shorts"

HOW IT STARTED. Back in late June, we introduced two Playbooks to guide our trading:

“ROTATION” Playbook: We asked ourselves, “What If” the Market rotates from the Winners to the Losers? We called this “The Pain Trade”, for the simple reason that most Monkeys are Momentum Monkeys that can’t tell Left from Right

“ELECTION VOLATILITY” Playbook: We called for Volatility to pick up in the Summer months, with a local Market Top sometime in mid-July. We titled the piece “Election Volatility”.

HOW IT’S GOING. Where we are now:

ROTATION: The Russell vs Nasdaq spread is up +13% in less than 2 weeks, one of the best relative performances EVER! The chart below shows the 5-day rolling performance of the pair since 1990. We are at levels of outperformance that occurred back in 2000…I can’t believe those pesky 2000-parallels are coming back again, I wonder why…

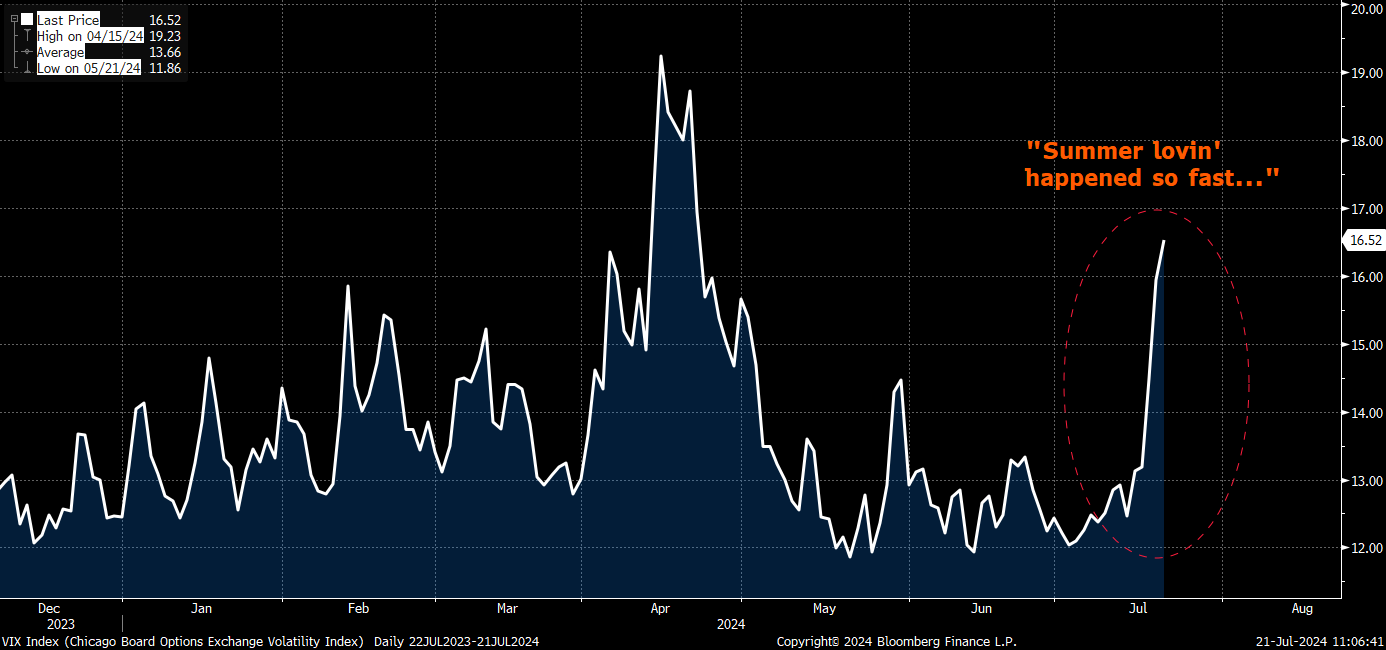

RUSSELL VS NASDAQ ELECTION VOLATILITY: This week, the Nasdaq lost 4% and the VIX jumped from 12 to 16! Meanwhile the S&P topped out on July 16th (!) and it’s now 3% off its all-time-high. Summer Volatility arrived like a clockwork … orange (pun intended!).

Where do we go from here?

Part 1. Technicals

On July 10th, we called for an “unwind” of the July “pump” in the Nasdaq, which was flow-driven in nature. We are now there, with the Nasdaq down 6% and back to levels last seen on …July 1st.

From now on, it gets tricky: