Yield to Immaturity

Europoors can't get nice things

I really hate technical analysis on things like Yields, the VIX or even Unemployment (groan). So it’s only fitting that I start this monologue with a chart of the US 10 year yield. It seems to be have bounced off the 100dma and maybe the 4.444% level is a little bit of a resistance for now.

Regular readers of my Twitter rant will know that I have a little bit of a thing for the number 4 this year which will continue into next year, with a possible climax on 04.04.2024 !

While Americans have been binge-eating during Thanksgiving (unless they are all on Ozempic by now), the Europoors have been a bit busy making a bit of a mess in the bond market:

The UK economy surprised to the upside with better PMIs but also sticky inflation. The UK Treasury had to respond of course with tax cuts and the Bank of England had to respond of course with a hawkish tone to play down the possibility of rate cuts. Which is of course what any half-respectable Emerging Market would do!

Zee Germans suspended the “debt brake” for 2023 (a German version of the Debt Ceiling with less fireworks). This is the 4th year in a row that this happens. And earlier in the week, Germany's Constitutional Court curbed the use of off-budget special funds (€100s of billions!), thus making the country’s fiscal outlook more uncertain

For zee Germans, the irony is that the trigger for the crisis was “the constitutional court’s decision to block a government move to transfer €60bn of unused borrowing capacity from its pandemic budget to a “climate and transformation fund” (KTF) that finances projects to modernise German industry and fight climate change.” Basically, ESG did it .. again!!!

Now regarding Germany, I’m sure there will be a lot of exaggerated comments but lets be clear, it’s a serious country and a serious economy (shame about the food).

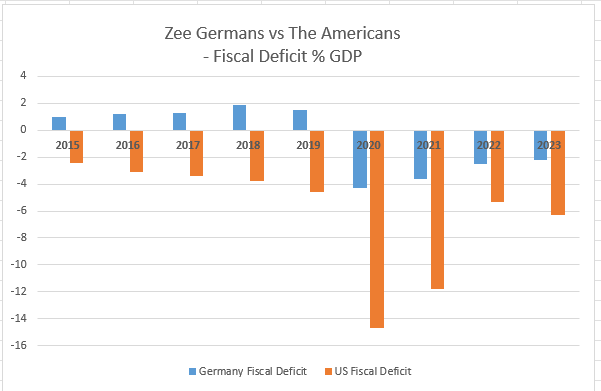

Compare the fiscal deficit of Germany vs the US and you can see a lot of years of surplus for Germany vs zero for the US. I don’t think the word “fiscal surplus” even exists in the US dictionary! Even during Covid, Germany had 4.3% deficit and the US had a 14.7% deficit! Talk about orders of magnitude of printing …

Which all comes round to concluding the following:

a) The UK and Germany don’t matter that much for the path of the Bond Market. It’s the US that drives the show, and we are just waiting for them to come back on Monday and sort things out

b) Mini Yield Tantrums will be a feature not a bug going forward. The market has been too accustomed to low yields that it assumes we will go back to 0% asap. We will not. Get used to it.

To clarify, I think we peaked in yields already. But given the politicians’ eagerness and anxiety to print and spend, I don’t think we can have a straight line path down to lower levels just yet. A US 10 year in the range of 4.0% - 4.444% is good enough for now!

Wishing you all a great weekend!

Disclaimer: Nothing here is investment advice, this is the trading blog of a shrub, this is parody, I could be in my parents’ basement trading for all you know, don’t be stupid!

True, but that's the old Germany. All those years of "fiscal surplus" will be reversed!

The only advice I think I got from this post was to avoid a certain country's culinary offerings. Noted. Won't be stupid.