Volcker, Trichet and Maverick walk into a Bar

The Fed Conundrum: to cut or not to cut

This is a post about the Fed’s choices regarding rate cuts. Therefore this is a macro post. Whenever a shrub writes a macro post, you are better off to just scroll on Instagram. Yea it’s that bad. But here is goes anyway:

The way I see it, the Fed has 2 choices:

Choice A: “TOP GUN: we will stir this bad boy to a soft landing”

Let’s not forget that 2024 is an Election Year. The focus is now inflation but the focus could easily turn to Unemployment

Under this scenario, as soon as the Fed sees unemployment pick up, and as long as inflation trends lower, they will cut

Under this scenario, on the FIRST CPI print with a 2% handle, they will be anxious to cut rates

This may well be by Q1 2024, as per Ackman comment

Choice B: “VOLCKER’S GHOST: We will kill Inflation Until no More”

Under this scenario, they acknowledge that Inflation is like a fungus that’s tough to kill or like that annoying relative that comes for a visit and ends up staying for the summer

In this case, the Fed would want to see CPI at or below 2% CONSTISTENTLY for a few quarters

Any self-respecting EM country would go down this route because they’ve been plagued by inflation too many times (see Brazil as an example). But the US isn’t EM so lets not get too zerohedge-y here ;)

When faced with such a macro dilemma, the question I ask myself, that has saved me money and stress is:

“WHAT DOES YELLEN WANT?!”

(If you think I’m joking I tweeted this before the October QRA decision when everyone expected a hawkish QRA and Yellen spanked the shorts like a German Dominatrix!)

Yellen obviously wants a Soft Landing. But lets pretend that the Fed is independent and that Yellen has no influence on the Fed. Of course, this is a fairy tale for kids but lets just go with it for the sake of some faux intellectual analysis.

In order to get an answer to my question, I went back to history to see how long the last rate pauses lasted. I went only as back as 1998 to check the last 3 pauses, partly because I was alive during those 3 periods and partly because I can’t be bothered to check what happened during the medieval ages. Also, I’m a firm believer in Recency Bias both for investors and policy makers (See how I turned a joke into actually a very serious point for further thought?!).

So here are the 3 pauses:

2000: Pause lasted for 8 months at a 6.5% rate

2006-2007: Pause lasted for 15 months at a 5.25% rate

2018-2019: Pause lasted for 7 months at 2.50% rate

Which brings us to today. We’ve had a pause for 4 months and at 5.5%

If this is 2000, then we are getting a cut by March 2024 and If this is 2006-7, we are getting a cut by Q4 2024.

Another observation: In all 3 cases, we had A LOT OF CUTS after the pause and the trend was a one-way street down to a lower level of 0-1% . So the TREND is DOWN. And FAST.

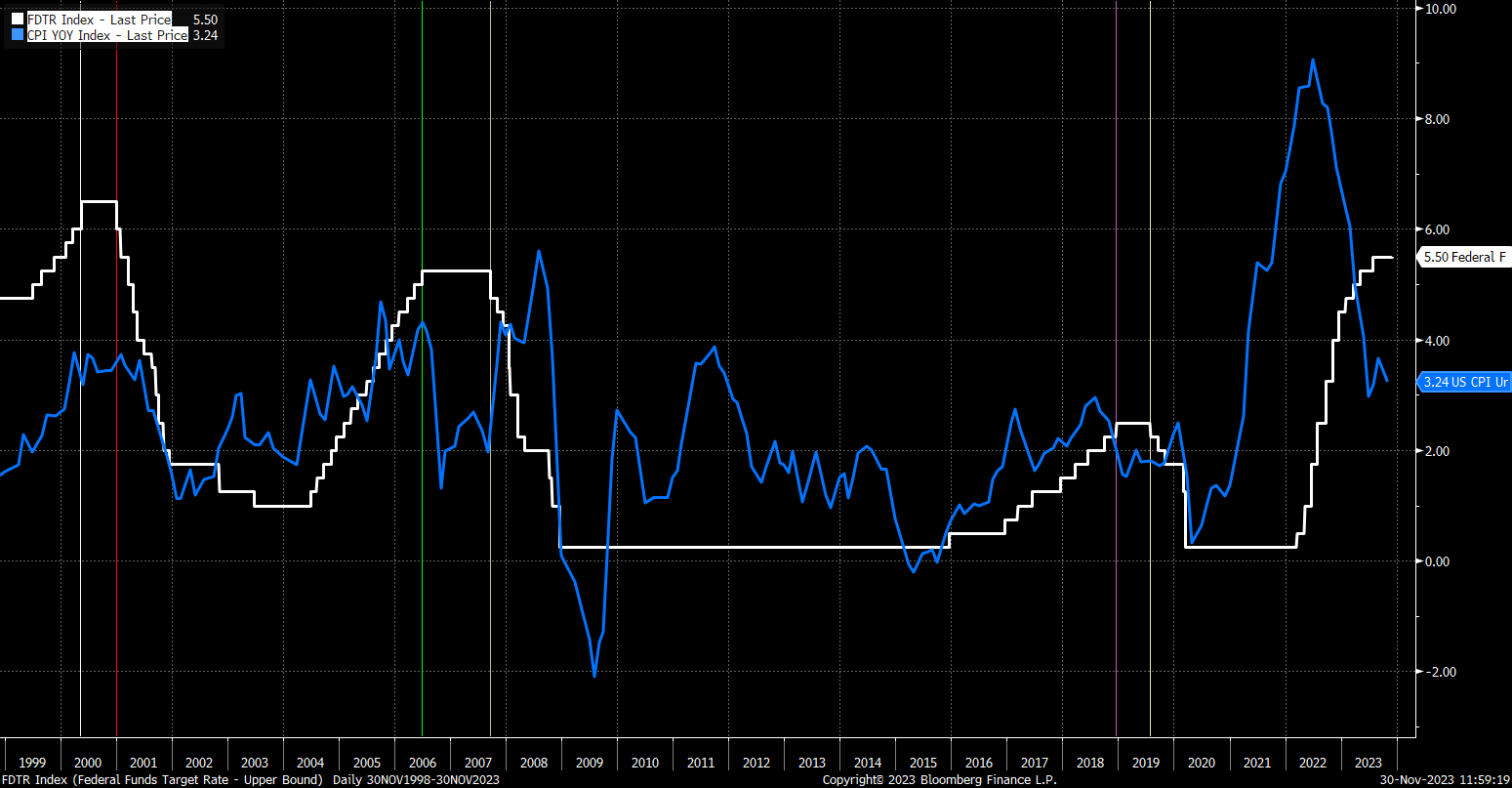

Lets superimpose Inflation on this chart to show the interplay between inflation and the Fed’s decision making at the time:

In 2000, Inflation was just below 4% and wasn’t really the issue and kept dropping to 2% even as more rate cuts were taking place.

In 2006-07, Inflation dropped from 4% to 2% during the Pause. Interestingly, it spiked in Q1 2008 to almost 6% but the Fed kept cutting.

In 2018, inflation was tame at 2% (because it’s a made-up number anyway).

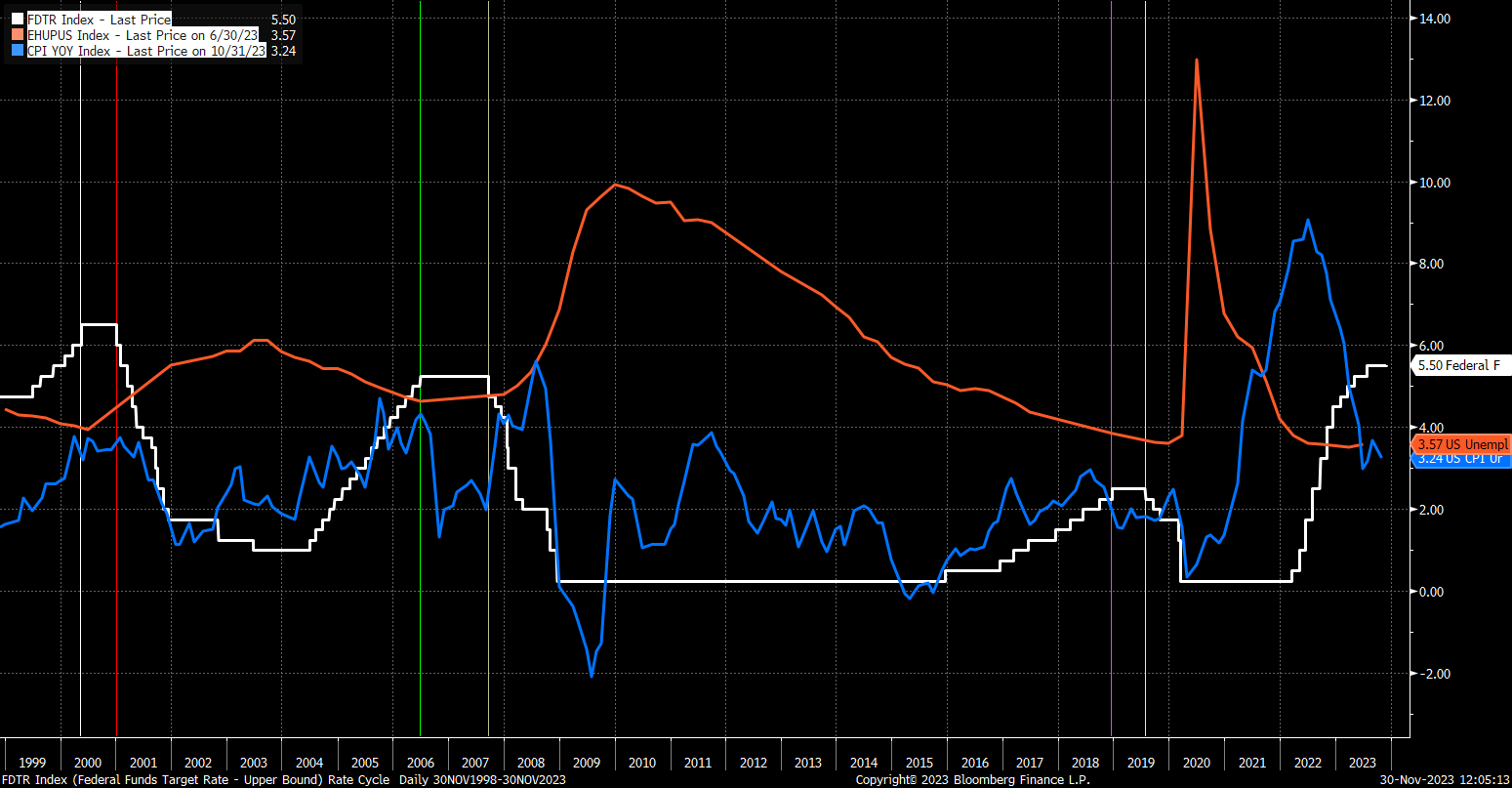

I’m still not getting a good answer to my original question, so lets also superimpose unemployment (red line) on our chart and see if we get somewhere:

Well that’s better … At least this shows the interplay between Unemployment and Fed rate decision.

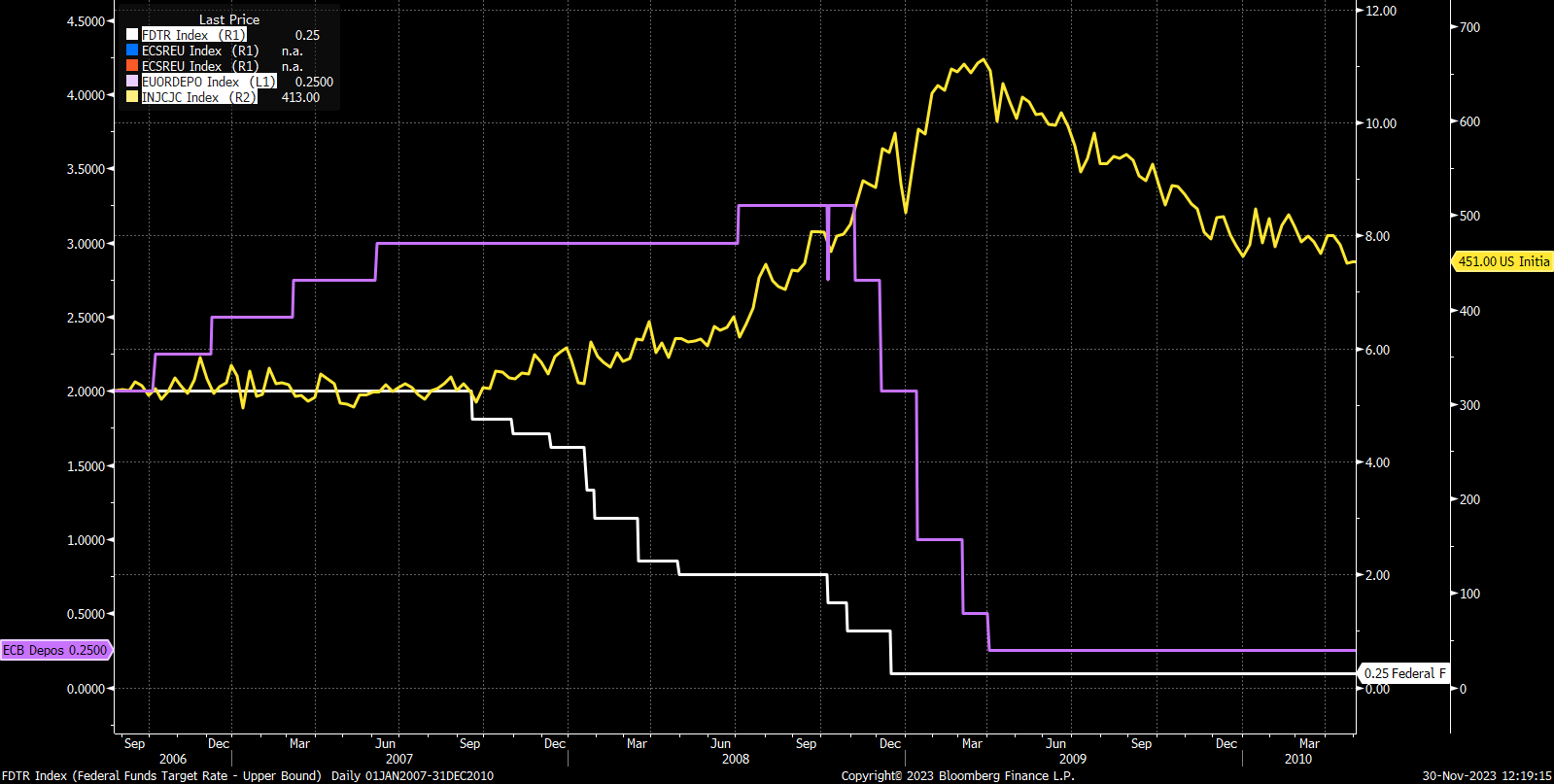

My pal KKGB Kitty has been banging on about tracking Initial Jobless Claims in order to decipher the Fed’s policy path.

So I zoomed in for 2000 and 2006-7 et voila (pink line below). As soon as there was a pickup in Initial Jobless Claims the Fed knew they had to pay attention.

I know that the discussion will inevitably lead to the question: “What if this is the 1970s!!”. To which I will bring back the new expression we learned today: “Recency Bias”.

Instead of asking “What if this is the 1970s and the Fed needs to act more like Volcker?”, I think the policy makers will be more likely asking “What if this is 2008 and we SHOULDN’T act like Trichet?”.

The old readers will recall that while the Fed started cutting rates in September 2007 (white line), and kept cutting as Initial Jobless Claims were rising (yellow line) the ECB kept rates high (violet line) until Xmas 2008 because of concerns around inflation!

What does that Mean for the Equity Markets?

Well, I don’t want to spoil everyone’s Festive spirits so I won’t tell you how the story ended in 2000 and 2008. You can pull up the charts for yourself.

But I will note from the charts above, that even though the Fed was cutting rates, unemployment kept rising … People always forget that the economy is a Tanker, not a dinghy …

Summary for Traders with ADHD

I know this has been a lot to digest for most of you (including me) so here’s a little recap:

Pauses aren’t forever

Once the Fed starts cutting, it keeps cutting

Initial Jobless Claims are a good early indicator for when the Fed will start cutting rates

Everyone thinks that the Fed’s biggest fear is to become Arthur Burns, but when the going gets tough their biggest fear is to become Trichet

Recency Bias is a cool concept. It affects both Investors and Policy Makers alike

Rate Cuts are not necessarily bullish for the Stock Market unless you believe that Jerome Powell is like Maverick from Top Gun

And never forget: “What Yellen wants, Yellen gets”. In which case, maybe the role of Maverick isn’t supposed to be played by Powell but by Yellen herself!

Janet Yellen, Top Gun pilot for the Economy! Anyway, here’s an exclusive photo of Yellen for you lovely Shrubstack subscribers ;)

Disclaimer: Nothing here is Investment Advice. This is the trading blog of a Shrub. This is Parody. Seriously, Don’t Be Stupid.

This is my favorite part of that writeup. Underrated comment...Excellent job, Shrub.

"To which I will bring back the new expression we learned today: Recency Bias”.

Good stuff, I guess I should keep buying 2's.