Ten Years Gone

History something something something

“Then, as it was, then again it will be,

And though the course may change sometimes

Rivers always reach the sea”

Ten Years Gone, Led Zeppelin

What a song. And how appropriate for the current CRE crisis. It’s quite amazing how this CRE theme cycled from being a headline story to a Page 10 story back to a headline story in the space of just one year (This latest Shrubstack is a follow-up from “SVB is dead, Long live SVB!” and “2 in a row”).

The headlines that just came out are again all too familiar:

“ NYCB Cut to Junk by Moody’s as Stock Hits Lowest Since 1997”

Thank you Moody’s for keeping us all safe with a post-facto downgrade! At least Moody’s adds a little bit of value by highlighting that NYCB doesn’t have enough reserves against its loans for multi-family, given these reserves are only … 1% of the loans. We are going to need a bigger boat! No wonder that NYCB’s chief risk officer left weeks before the big loss :/

And Zee Germans are at it again! Last week it was Deutsche Bank, this week it’s the unpronounceable Deutsche Pfandbriefbank (lets just call it buy its ticker: PBB). This headline popped on Bloomberg so you know it’s getting serious:

“German Regulator Is Monitoring Commercial Real Estate Turmoil”

PBB has roughly €4bn of US CRE exposure, which is equivalent to their total Equity so obviously it draws attention. Their bonds plunged after Morgan Stanley told their clients the obvious: “PBB has US CRE exposure!”. Since none looks at balance sheets or does mafs anymore, they needed Morgan Stanley to tell them, so the credit monkeys proceeded to sell the PBB bonds and every other German banks’ bonds with a hint of US CRE exposure, creating a mini-turmoil within the obscure corner that is the German Bank Credit market.

This CRE / Multi-family drama is just unfinished business from 2023. And whether rates stay at 5% or go to 0%, at some point this business will be dealt with (“And though the course may change sometimes, Rivers always reach the sea”). Powell himself said that CRE “feels like a problem we’ll be working on for years”.

The chart below from Petrus Advisers shows that it typically takes several years for US CRE asset quality to really deteriorate. So imagine being back in 2007 and seeing low delinquencies and getting bulled up on CRE when the obvious blow-up was staring you in the face (“Then, as it was, then again it will be”)

Given this Shrubstack is titled “Ten Years Gone”, it would be remiss to not mention the US 10 Year Treasury.

I see a lot of smart people calling for a re-acceleration of inflation and shorting Duration ie shorting the US10yr.

I get it. But once again, are we seeing re-acceleration of Plebflation or are seeing re-acceleration of Wealthflation? I see mostly the latter for now (NVDA to the moon!), though I’m aware eventually it will feed into the Plebs. But this takes a bit of time. Will it be H2 2024 or will it be 2025? It’s anyone’s guess.

But on the other hand, we just spent the first part of the Shrubstack talking about CRE / multi-family implosions. The last time this happened in March 2023 the US 10 year touched 3.3%.

So with the US 10 year at 4.1%, do I really want to be short duration? I’m basically short the tail risk of another mini-credit crisis and I’m short a downward trend in inflation (whether it settles at 2% or 3% who cares for now).

But I’m not that bullish duration either. We know that the Tamagotchi is out of control, so with a few trillion of issuance, I can see this just staying at 4-4.5% for a while.

In summary, I don’t think shorting or going long duration is a great trade at this point. Feels like 1 up 1 down kinda thing at best, either way. I actually don’t care on it at this level :/

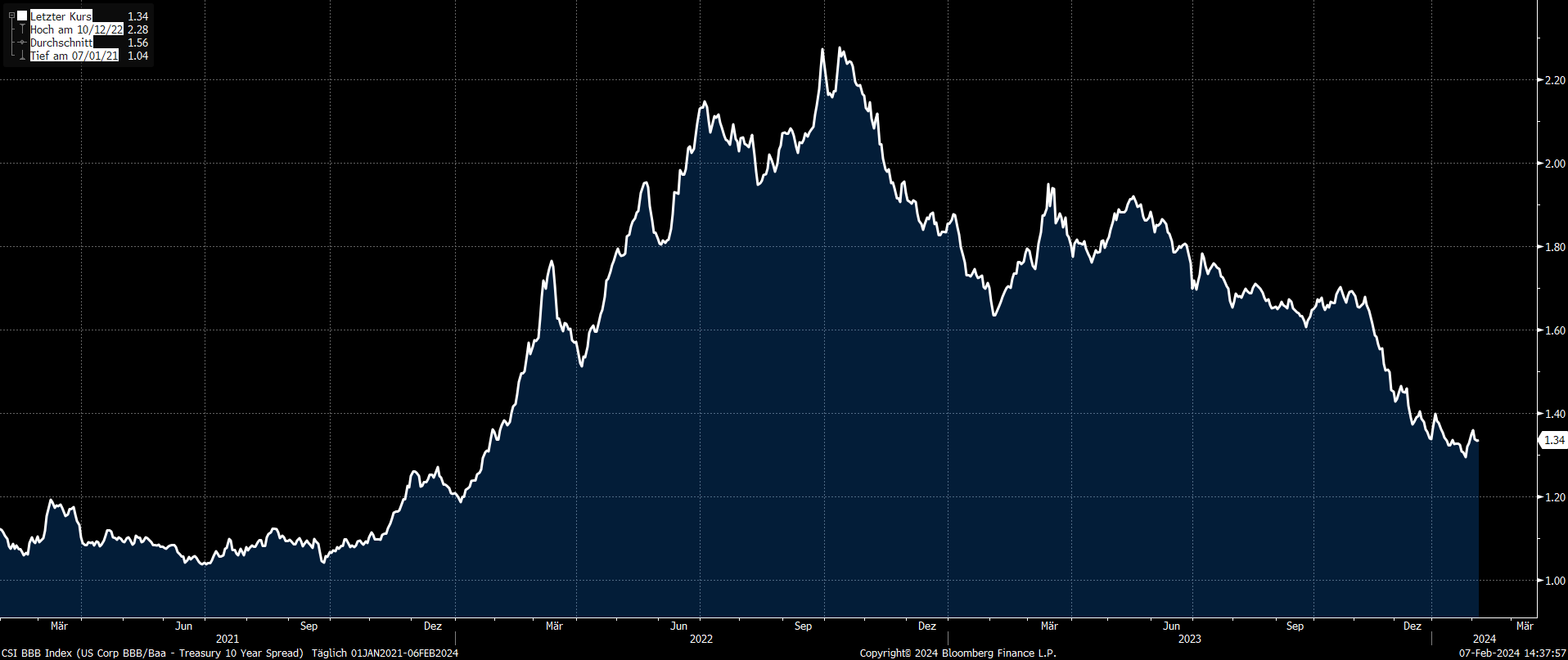

A smarter trade, and unfortunately one that’s tough to set up, but with MAJOR implications for all portfolios, is to observe the credit spreads RELATIVE to the US 10year right now:

The first chart is the spread of the BBB bonds relative to US 10 year Treasuries. In March 2023, it was nearly 200bps spread and now it’s 134bps. The lowest it’s been was 100bps in 2023. So we are near the tightest credit spreads everrrrrr

The next chart is the spread of the Barclays High Yield Index relative to the US 10 year. This is 375bps and was 560bps in March 2023. The lows were in 2021 near 200bps. Same conclusion.

This is a much better short than the US10yr as it’s asymmetric with low downside risk. You don’t lose sleep whether a bank goes bust overnight. In fact, if a bank goes bust overnight, this spread blows up again and you make a ton of money.

But it’s also tough to set up. So here’s how to use it as signal instead: If the spread blows up, you kinda don’t want to be long Russell / mid-caps / levered cos etc.

Below I plotted the Inverse Russel vs the BBB Credit Spread (from above). You can see a pretty good correlation. In fact the correlation would suggest the Russell should be higher given how tight the spreads are (ie the inverse Russell should be lower). So maybe the Russell is smelling the rot already, or maybe the spreads are about to blow up again or maybe both.

My point is, Credit Spreads are what you want to be keeping a track on from here on.

We are past the “INTEREST RATE RISK” phase and we are entering a “CREDIT RISK” phase, even if it’s just for a small subsector of the market. And I care about this small subsector since my shorts are concentrated here!

So keep an eye on the spreads. They are the ones that will dictate the direction going forward. And listen to “10 Years Gone”. Just epic.

Disclaimer:

This isn’t financial advice. This is the equivalent of reading MAD magazine but for finance but worse: This is the trading blog of a shrub.

Don’t be Stupid. Seriously. How many times do I have to repeat this ….

Another masterpiece! I agree that credit spreads and a few other factors look veryyyyy compressed. Entertaining and instructive piece as always! Thank you!

Great read Shrub 🙏