One Last Yolo - Star Wars Edition

"The Theory of Rolling Ponzis" gets put to the test once again!

The Memes are getting sillier, so this HAS to be the last “One Last Yolo” for 2025…

With Space-X about to IPO in 2026 and Trump recently issuing an Executive Order to “Ensure American Space Superiority”, the Space Sector is set to go to the Moon in 2026 (pun intended). Therefore, it’s only fitting that we end the year with a Space Ponzi as a “last Yolo”.

I really wasn’t sure If I was going to write this one up, but it’s so ridiculous that only a parody publication can do it proper justice:

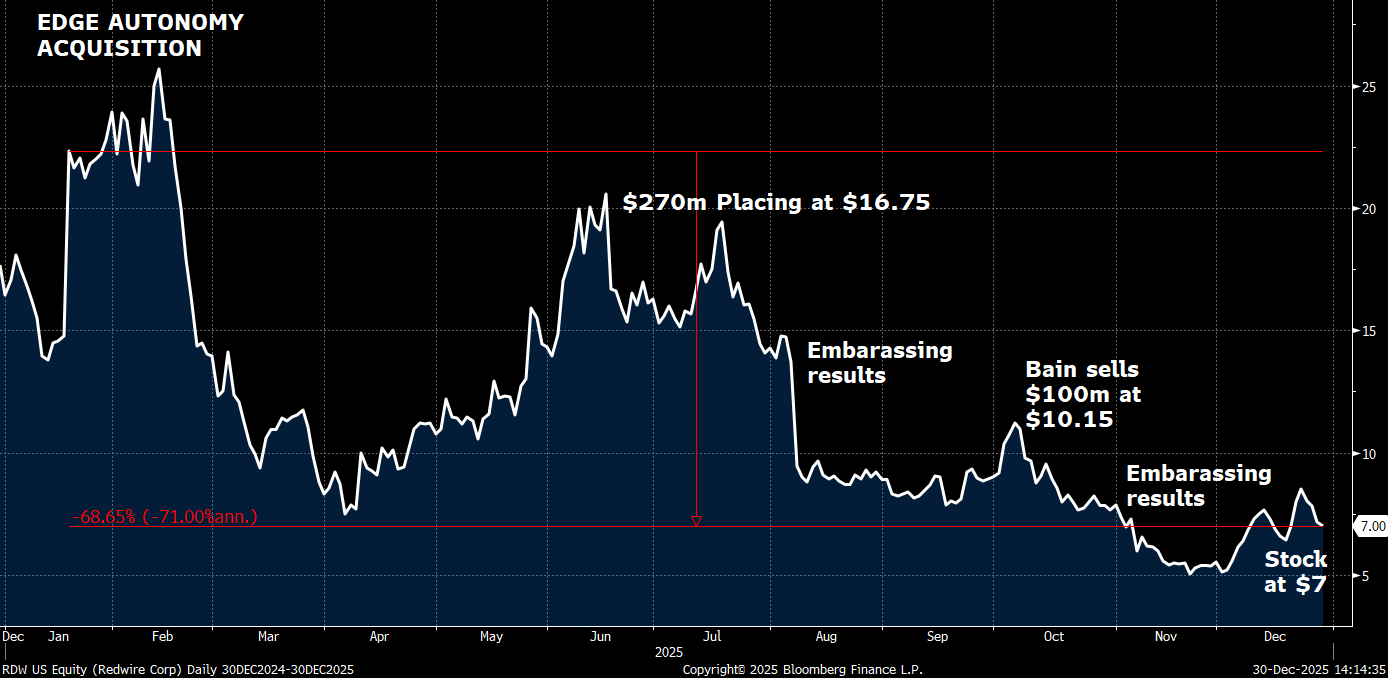

The company is Redwire (ticker: RDW), a $1.2bn market cap company, majority-owned by Aerospace private equity firm AE Industrial Partners.

The company is a hodgepodge of space assets, put together by AE Industrial Partners in 2020 and IPO’ed via a SPAC in 2021. To make it even more complicated, in January 2025 RDW bought drone company Edge Autonomy from … AE Industrial Partners.

I hate this type of related party transactions. Red Flag🚩!

RDW paid $925m for it, of which $150m in cash and rest $775m in stock with a VWAP of $15 per share i.e. 2x higher than today’s share price.

To make it worse, the company had a series of the worst earnings prints I’ve come across, plus a decent-sized seller (Bain):

August 2025: Sales came in at $62m vs $95m estimate! EBITDA came at a loss of -$27m vs +$6m estimate! The company blamed “uncertain timing of Government Contracting” due to the government shutdown and had to lower FY2025 Sales Guidance from $535m-$605m to $385m-$445m. Embarrassing stuff! The stock closed down 30% on that day.

October 2025: Bain sold out $100m of stock at $10.15

November 2025: Earnings miss again! Sales came in at $103m vs $129m estimate. Stock closed down c.20% that day

Investors got really burned from this company and the management credibility is pretty low. In particular, a couple of days before the August results, CEO Peter Cannito was interviewed on Fox to discuss the company’s new venture, SpaceMD, which was focused on drug development in space using their microgravity platforms. Everything looked rosy. A couple of days later, results came out and … rugpull!

I can’t infer an opinion on the CEO but geez man … if you know you are going to miss revenues by >30% in a couple of days time a) You don’t go on TV to talk about your next moonshot venture, b) You pre-announce! The company therefore suffers from severe lack of management credibility. Red Flag🚩

In November, the CEO had the half-decency to buy $250k worth of stock at around $6. That’s something.

Furthermore, after the Edge Autonomy acquisition, the Balance Sheet isn’t that great, with $174m net debt and c.$220m in convertible preferreds (c.$100m at book value). For a cash-burning company, that’s too much. Red Flag🚩

There is a good chance that RDW will need to raise capital in 2026. They do have an Equity Distribution Agreement (ATM) already in place, which they probably have put / are putting to use since it’s actually a pretty liquid stock which trades >$100m per day.

Incidentally, the short interest on the stock is c.30%, which is probably the most bullish thing I’ve said about the company so far.

Ok, enough with the red flags. Lets spell out some of the good stuff:

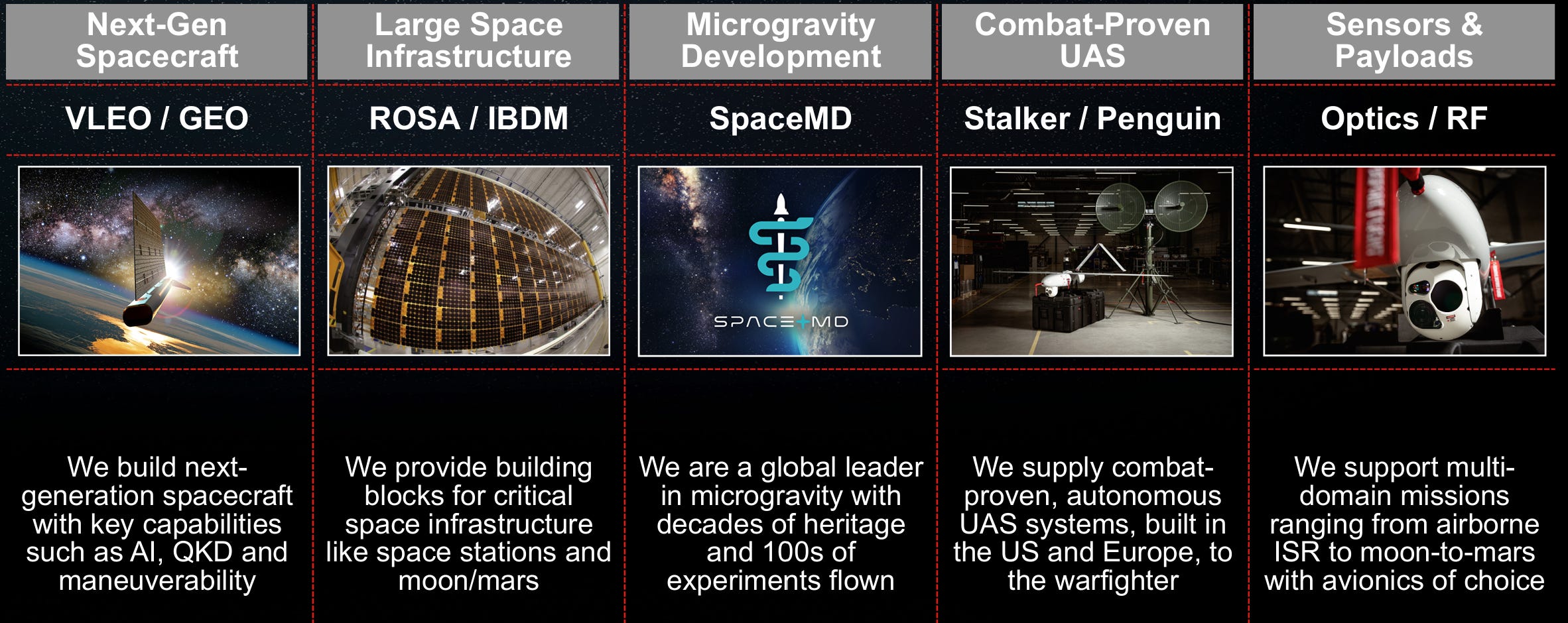

What Does the Company Do?

As we said earlier, the company is a hodgepodge of space assets + a drone company, but that doesn’t mean they are not valuable or interesting. In fact, some are impressive:

VLEO: RDW is the first mover and leader in VLEO spacecraft (Very-Low-Earth-Orbit). VLEO is interesting as the satellites are closer to the ground than LEO, which improves operational efficiency (e.g. lower latency). RDW has developed specialized "air-breathing" electric propulsion systems that use the thin atmosphere itself as fuel to counteract drag.

RDW is already the prime contractor for the European Space Agency’s VLEO program & has been awarded a $44m contract to advance the Department of War’s DARPA VLEO project “to demonstrate the world’s first air-breathing spacecraft and advance next-generation orbital capabilities”.

Roll Out Solar Arrays (ROSA): RDW is the leader in lightweight solar arrays which are used to power satellites as well as the International Space Station.

SpaceMD: RDW makes space pharma labs called PIL-BOXes (Pharmaceutical In-space Laboratory) for “microgravity” development. This may sound silly, but there are already 42 PIL-BOXes on the ISS.

Edge Autonomy: The drone business is OK, with US Army contracts as well as being combat-proven in Ukraine.

Space as the next Rolling Ponzi

We introduced our “Theory of Rolling Ponzis” a year ago. In summary:

“The Market Monkey has a one-week horizon and will buy everything related to the Ponzi du Jour, before moving on to the next Ponzi”

- Le Shrub’s Theory of Rolling Ponzis

We have a successful track record of multi-baggers in Quantum Ponzis, Spinny Ponzis, Nuclear Ponzis and Drone Ponzis.

I guess it’s time for a Space Ponzi! It’s also time for a Meme:

Catalysts

A rolling Ponzi needs a catalyst to work. RDW has a few catalysts lined up for 2026:

SPACE-X IPO & Space Data Centers: Elon is trying hard to sell the Space-X IPO above $1 trillion so he miraculously invented a new category out of thin air: the Space Data Center. I have no clue if it’s feasible or not, but I do know that RDW makes the solar panels for the ISS, so at least as a narrative play, RDW can also have a part in powering space data centers. Once you realize it’s all nonsense, it starts to make sense, innit.

VLEO: The Executive Order on Space referenced above, specifically mentions VLEO capabilities development as a priority. Well, RDW is the leader in this:

Contract timing & Management Credibility: Recall that the big earnings misses were around contract awards getting delayed due to Government shutdown. The best way for Management to regain credibility is to actually get those contracts done! IF this happens, then the narrative changes, plus the credit profile will look better, limiting the need for further dilution. The equation will look like this:

Mgmt Credibility Up + Less Dilution —> less red flags —> Stock re-rates

Frankly, this may be the worst pitch ever, but I like to raise all the red flags upfront as it helps me in sizing (or avoiding the stock altogether). RDW firmly belongs in the “show me” / “Rolling Ponzi” bucket, so 1% NAV is OK - maybe 2% NAV if they get contracts done and / or raise again, preferably from a position of strength. Oversize this trade, or frankly any Rolling Ponzi, and you’ll end up like “Han Yolo”:

Good luck out there and May the YoloForce be with you <I’ll see myself out>.

🌳🙏

Disclaimer:

This isn’t financial advice. This is Parody. This is the equivalent of Monty Python for finance, but worse: This is the trading blog of a shrub. For all you know, I could be a 15-year old paper-trading out of my parents’ basement. Don’t be Stupid. Seriously. How many times do I have to repeat this.

Hey Shrub! always thankful for your witty comments and humor. You have the looks (according to Cit), the brains, the humor, and most importantly the heart at the right place. I look forward to the year 2026 with your write-ups and your stress free approach to the market. From the heart, thank you.

On the Space Ponzi, I will pass on RDW. I had it in the port for a while and we hated each other. So, following your simplicity philosophy I will go for RKLB, drink two or three gin tonic, and hopefully forget until end of next year about this purchase.

Happy New Year! 🎊

You forgot other catalyst. Partnered with Vast. They have some medical infrastructure thing on their ship about to launch in May. If successful expect more printing:)