Buying Emerging Market Sovereign Debt for pennies on the dollar

Venezuela is the definition of a basket-case EM. The country defaulted on $60bn of bonds in 2017 and the bonds have since been trading at pennies on the dollar. If that wasn’t enough, the US had also imposed sanctions in Venezuela since 2019 as a response to the Maduro regime’s repression of protesters.

Venezuela, however, has significant oil reserves and given the global geopolitical mess currently, the US reached out to get a deal done and get the “oil spice” flowing. Even though the Maduro regime isn’t exactly a poster child for human rights, the alternatives are way worse, to put it politely.

As part of the deal, the US has lifted sanctions on trading of Venezuela bonds and lo and behold, the bonds have almost doubled overnight to touch 20c.

I’m quite annoyed that I wasn’t able to buy the bonds before due to restrictions, but that led me down this rabbit hole:

Is there another Emerging Market (EM) with debt trading at pennies on the dollar?

And that led me to my favourite EM, the place I used to call home: the UK.

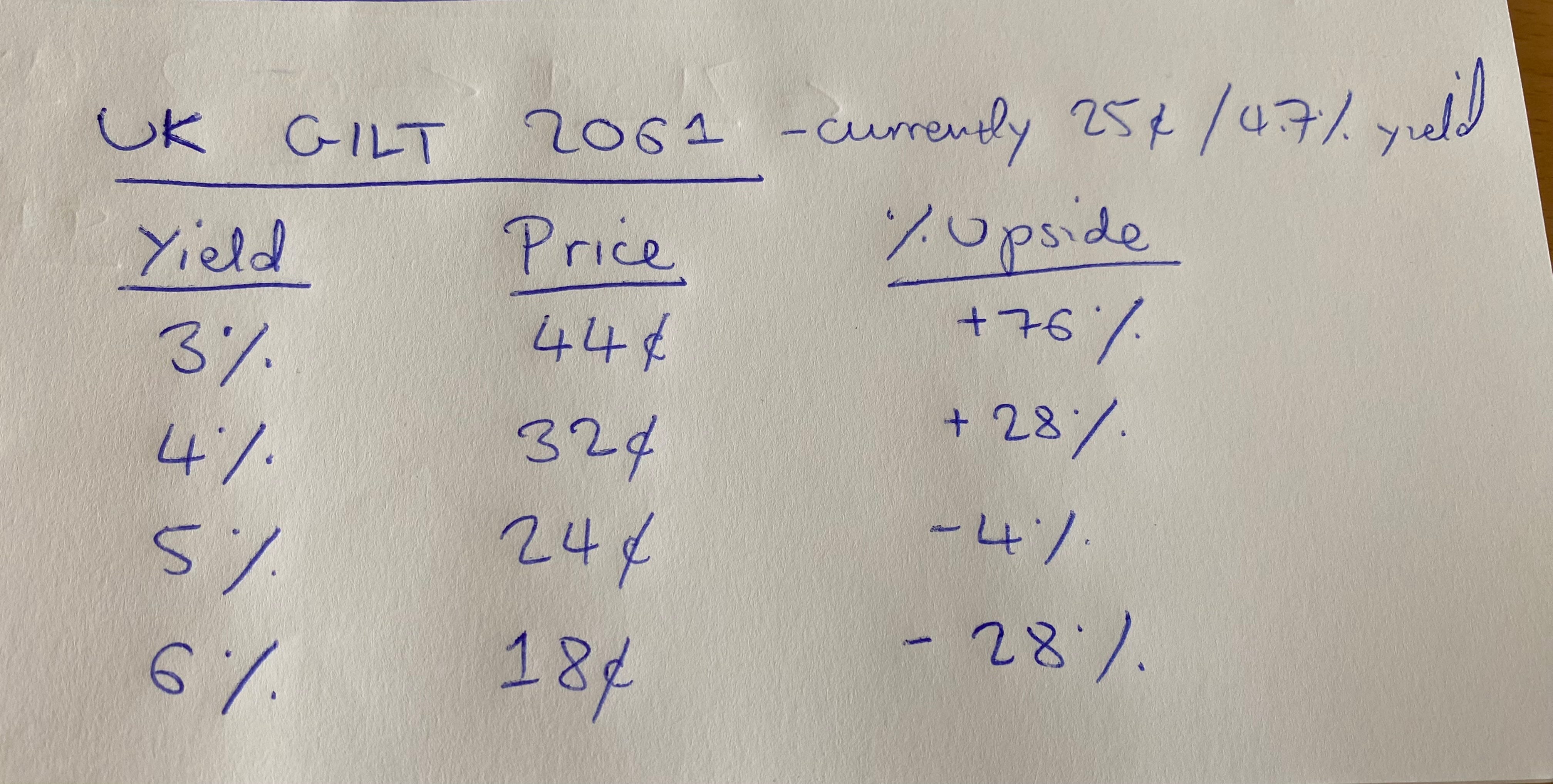

The UK issued a 2061 bond in the summer of 2020 at 100c with a very juicy coupon of 0.5% (!) and of course the pension funds couldn’t get enough of it back then. Unfortunately for them, this bond is now trading at 25c on the dollar. The pension funds lost 75% of their capital in 3 years in what was supposed to be their safest asset. Well at least they got 3 years’ worth of 0.5% coupons to offset the loss (lol!)

Incidentally, UK sovereign bonds are called Gilts. I think it has to do with the guilt that buyers eventually feel for owning a bond in such an inflation-prone country.

To summarize, let’s go back in time to the summer of 2020:

Had you put $100 in the safe “Developed Market” paper of the UK, you would’ve lost 75% of your money (white line below)

Had you put $100 in the risky “Emerging Market” paper of Venezuela, you would’ve almost doubled (blue line below)

Fast-forward to today.

I don’t have an opinion whether I should buy the Venezuela paper at 20c. But let’s look at the UK Gilt at 25c.

Incidentally, at the depths of the LDI crisis, the 2061 Gilt traded at 25c, pretty much these levels, and that was considered to be a disaster (Liz Truss was kicked out as Prime Minister because of that fiasco).

The running yield is crap at 2% (0.5% divided by 25c, for the mathematically impaired reader). But the yield to maturity is around 4.7%, which is ok-ish for someone who hopefully has another few good decades: a 4-bagger in 40 years, wooohooo!

So why even bother to look at this?

Let’s do a a pretty bad scenario first: UK turns to a proper “EM” and yields blow out to 6%. The Gilt will then drop by 28% and trade at 18c.

Now let’s do a base case where the UK returns to some basic level of “DM” credibility and trades at 4% yield: then the bond will trade at 32c and will be up 23%. Meh, ok,

But let’s say the UK goes into a recession. Or let’s say something else happens e.g., UK moves to fiscal prudence (or is rather forced to) or that “they” (aka Treasury / BOE) want the yields to tighten and the yields go to 3%. Then the Gilt will trade at 44c or almost a double. Better.

One can assign any probabilities they want on the different outcomes. I added a very complicated model for whoever wants to play with the numbers:

From my part, I had some GBP laying around and, since I consider them to be worthless paper anyway, I bought a 2% position in this and plan to sit on it for a while.

I prefer it to the US long-dated paper for various reasons: the UK pension funds actually buy this paper and there are tax incentives for UK people to own Gilts as the capital gains is tax-free, not a bad incentive for a near-certain multi-bagger (obviously none should ever listen to a shrub for anything, especially for tax advice – don’t be stupid!).

I want to start building longer duration exposure in my portfolio as I think we are entering the last innings of the cycle. I’m patient with the timing and I may address it in a later article. I already have a 5% position in US 10-year TIPs and now this 2% position in the 2061 UK Gilt to add spice to my duration trade, which hopefully won’t end up as Guilt. Time will show. At least I have 40 years ahead to find out :/

(If it feels like a stupid trade just think of the pension funds that bought this 300% higher and have a laugh about it)

Welcome to Substack, sir Shrub! Looking forward to reading your long-form thoughts. I'll share this article with my readers tomorrow.

Cheers

Great article! Interesting and hilarious at the same time ahahah.

For even higher convexity take a look at the Austria 100y, also better currency exposure imo. This one will really take-off in a lower interest rate scenario